While contract subrogation may sound like legal jargon, most of us have come across its usage — even if the term itself seems foreign or unfamiliar — at least once in our everyday lives.

Imagine you are driving down the road and suddenly someone runs a red light and crashes into your car.

Thankfully, you’re insured and your insurance company covers the damages to your vehicle as well as any injuries you sustained — that is an IRL example of subrogation in contract law being exercised.

Let’s dive deeper into the contract subrogation definition and why it’s crucial to understand how it works in various contractual agreements.

Key takeaways

- Contract subrogation is when one party (like an insurance company) has the right to “step into the shoes” of another party (injured individual) to pursue a claim for damages.

- Subrogation can be equitable, conventional, or statutory, each arising from similar but not identical circumstances related to negligence, contractual agreements, or legal statutes.

- A waiver of subrogation is an agreement whereby an insurer relinquishes the right to seek recovery from a third party for a loss paid to the insured.

- Waivers of subrogation in contract law help prevent lawsuits between parties by foregoing the right to pursue claims against each other for insured losses, thereby streamlining insurance procedures and enhancing financial security and recovery efforts.

What is meant by contract subrogation?

A right of subrogation in a contract occurs after one party incurs a loss or damage due to the actions or negligence of another party and the injured or affected party’s insurer steps in — exercises their right of subrogation, which we will detail below — to seek remedies from the party at fault.

Following the same analogy with car accidents, your insurance company pursues the other driver or their insurance company to recover the funds they used to compensate you.

The subrogation contract you have with your insurance carrier stipulates that they have the legal right — and contractual obligation — to seek and collect reimbursements in your place instead of just letting the at-fault driver off the hook.

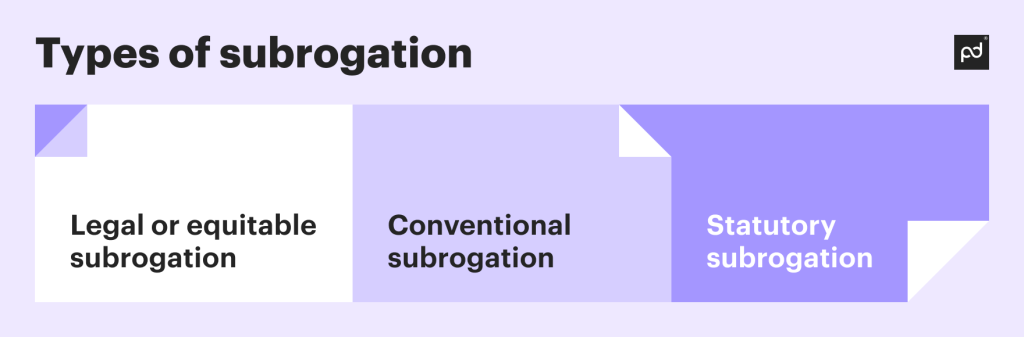

Types of subrogation

Legal or equitable subrogation

This type of subrogation arises by operation of law (rather than through an agreement between parties) when one party pays a debt or claims that another party is primarily responsible for.

It’s based on equity principles, aiming to ensure fairness by allowing the party who paid the debt to step into the shoes of the creditor.

Simply put, no contract is necessary for this type of subrogation

Example

Say you cosign for a friend’s loan, and they stop paying on the debt. As cosigner, you step in and settle the amount owed with the creditor. Now you can seek recovery from the borrower (assuming you’re still friends!).

Conventional subrogation

Conventional subrogation results from an agreement typically found in insurance policies, making it a subrogation in contract form.

It’s where one party agrees to have their rights transferred to another after a payment or settlement is made.

This is the most common form of subrogation, with stipulations outlined in a contract.

Example

A homeowner’s insurance covers damages from a fire caused by faulty electrical wiring, so the insurance company can seek repayment from the electrical contractor after paying the homeowner to get all damages fixed.

This is the conventional type of subrogation, as it is based on terms outlined in the insurance policy contract.

Statutory subrogation

Statutory subrogation is granted by specific laws or statutes that automatically provide the right of subrogation to certain parties under particular circumstances.

This does not depend on contractual agreements but on legislative enactments.

Example

Compensation laws may grant the worker’s insurance company the right to seek repayment from a party responsible for an employee’s injury — the insurer’s right to seek remedies and the process involved are governed by the specific provisions known as “workers’ comp” laws or regulations that fall in line with the rights of employees.

What is a waiver of subrogation?

A waiver of subrogation means that an insured party agrees not to have their insurer claim damages or obtain reimbursement from another party or the other party’s insurance company.

In case of any losses occurring that would otherwise be covered under an insurance policy, it’s like saying: “If there will be any fault, whether yours or partly yours, neither I nor my insurance company is going to come after you.”

Why would anyone waive their rights like this?

If we use the same car accident analogy, say the person that hits your car doesn’t want to use their insurance to cover the damages they caused (filing a claim will likely raise their insurance rates).

In this scenario, if you agree to settle with the at-fault party directly and on your terms (neither party’s insurance is involved), then you would sign a waiver of subrogation so your insurance company can’t legally seek remedies in your place.

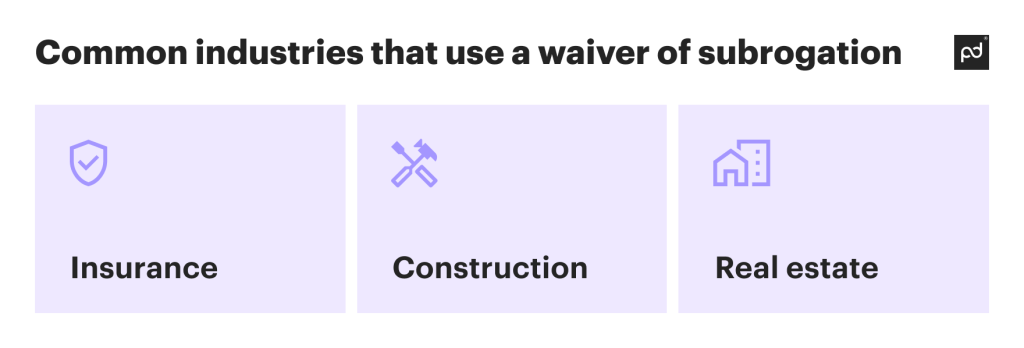

In several industries, waivers of subrogation are often used in commercial insurance policies with the goal to simplify the relationship between two parties in a contract.

In construction contracts, for example, using subrogation waivers also helps involved parties — owners, contractors, and subcontractors — reduce their risk of being involved in endless lawsuits against each other should any accidents occur.

How subrogation works in an insurance policy

Subrogation is common in the insurance sector, and involves three parties:

- The insurance company

- The policyholder

- A third-party responsible for the damages

The process of subrogation starts with a policyholder claiming for the damage cost incurred in an accident that happened because of the third-party.

Once the claim is settled with the insured person, the insurance company acquires the insured’s right to recover the amount from the party responsible for the loss.

This allows insurers the legal rights to seek reimbursement from the at-fault party.

What does “right of subrogation” mean?

As noted above, the right of subrogation means that if your insurance carrier compensates you for a claim, they have the legal right to go after the person or party responsible for the damage to get their money back.

Think of it as your insurance company standing in for you, seeking to recover the funds they paid out.

And since the insurer has the right of subrogation, they can also initiate a lawsuit to recover damages they paid in your name — just as if you were bringing the suit yourself in case the at-fault party (or their insurance carrier) doesn’t want to voluntarily pay for the damage.

How subrogation works in lease agreements

Subrogation clauses in lease agreements determine which party is responsible for losses or damages to the rented property, or to the individuals while inside the property. (Note: Always understand exactly which rights you waive when signing during the rental application approval process.)

Generally speaking, if something happens to the property that is the homeowner’s or landlord’s responsibility — like faulty wiring that caused a fire in a tenant’s apartment — the owner’s insurance company covers the cost of repairs or replacement without being able to make an insurance claim against the tenant or their insurer.

However, if a guest is visiting the tenant’s apartment, and that guest injures themselves at the property, the guest will be suing the tenant’s insurance carrier — and that’s it.

The tenant / tenant’s insurance company will not be able to then sue the landlord to recover whatever was paid out in damages because of injuries sustained by the guest.

How subrogation works in construction contracts

In the construction domain, when damage or injuries occur, all parties involved (contractors and owners) have insurance coverage to handle such incidents.

Commercial construction contracts include numerous clauses, with indemnity (“holding one harmless”) being a major one — when unplanned events happen, who assumes responsibility must be well-defined at the onset.

In a similar vein, subrogation clauses make it clear who is responsible for what — and therefore which insurance carrier is liable — should accidents or damages occur, thus preventing parties from suing each other to recover costs.

Here’s one example: If a contractor’s negligence results in flooding out several floors of a building under construction, and the project owner’s insurance covers the property damage, the insurer’s subrogation rights will be employed to recover those costs from the contractor or their insurance carrier.

Subrogation in construction guarantees that insurance companies work to recover costs, while signing waivers of subrogation clauses help distribute risk among the various parties involved in construction projects.

When is a waiver of subrogation needed?

With the main goal to contain a financial loss to a specific party’s insurance policy in order to help control costs and manage risk, a waiver of subrogation is needed to:

Protect parties from potential lawsuits

Either one or both parties (in case of mutual waiver of subrogation) agree not to pursue legal claims against each other for damages that will be covered by insurance policies.

Reduce legal disputes

A waiver of subrogation prevents conflicts and disputes between parties by clarifying that insurance companies will be responsible for handling claims and recovery efforts.

Simplify insurance processes

Subrogation clauses help insurance companies to speed up and simplify the recovery process by reducing the need for additional legal action or involvement from the parties.

Grant financial protection

Waivers of subrogation ensures that parties aren’t held financially responsible for losses or damages covered by insurance policies, reducing potential financial risks.

Create a legally valid waiver of subrogation in minutes

PandaDoc offers online waiver software that allows you to create a legally valid electronic waiver in just a few minutes — no wasting time on outdated methods or inefficient systems to produce these important documents.

The process is simple: you just create a template or choose one from the PandaDoc library, select the preferred option on how you want to share the form and take advantage of using e-signatures to speed up gathering all signed waivers.

Our platform facilitates fast, paperless and secure solutions powered by comprehensive document management software.

And storing all contracts within one safe digital repository enables transparency and engagement, allowing quick retrieval of docs so all parties can effortlessly communicate and easily share files or contracts.

Start a free trial or schedule a demo to leverage PandaDoc waivers today!