If you’ve been on the internet long enough researching invoices, the one common element you’ve likely found while clicking links is that your invoices should have payment terms (also referred to as “payment terms and conditions”).

The logical question you may very well have asked yourself after this is, “What on earth are invoice payment terms and conditions?”

So, here’s the short answer: They are terms of payment a seller puts on an invoice.

TL;DR: Payment terms (“invoice terms and conditions”) is essentially a list of terms you mention about how you’d like to get paid. For example, do you expect to receive payment in 7 days? Do you expect payment by check? Do you have late fees? Etc.

If you’re seeking a longer, more comprehensive answer, you need look no further than reading this article, because we’ve got it all covered. Sounds good? Let’s get on with it!

What are invoice terms and conditions, and what are the different types?

Suppose you’re part of the accounts department in a company.

You’re living your best accountant life, filing away financial documents, being on top of bookkeeping, networking with colleagues, and so forth.

Suddenly, one fine day, you get an invoice from a vendor — it only has their billing address, invoice date, the list of tasks they did, and the total amount due.

You’ve got thousands of tasks on your to-do list, and so you think maybe you’ll get to the invoice at the end of the week —- no worries, right? Right?

Well, as it turns out, the invoice required immediate payment, and now you have to process an additional late fee along with the invoice amount.

This sounds like a lose-lose situation for all parties.

The client has to pay an additional amount, and the vendor has to wait for extra days to be paid, even though they had a contract stipulating that there should be no late payment.

So, what can be done to negate this situation entirely? Well, you can add payment terms.

What are invoice terms and conditions?

Invoice terms and conditions are the guidelines a seller will include on an invoice. They specify how and when payment should be made, what payment methods are accepted, and if there are any fees or penalties for late or missing payments.

These terms and conditions are intended to set expectations for both parties while outlining any obligations like due dates, discounts, and charge-backs. They also help avoid misunderstandings, which can result in a delayed payment or even disputes.

Essentially, these terms make for a smoother, more predictable financial transaction between parties.

When we speak of payment terms and conditions, there are two types of formats one can refer to.

Format #1

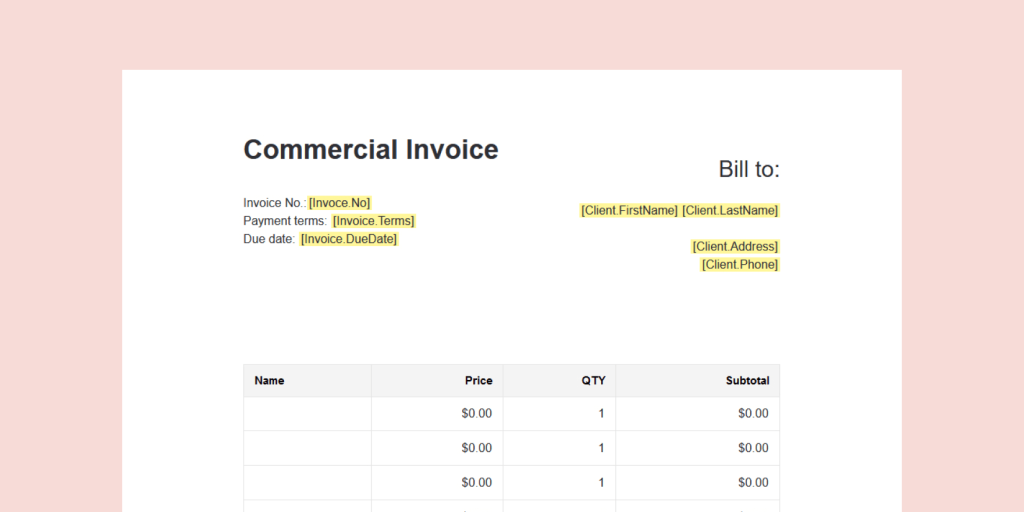

The first format is short and sweet. It lists down the basic stuff, such as the payment due date, late fee charges (if any), and what kind of payment methods (e.g., cash on delivery, credit card, check) you prefer. It looks something like this:

While not compulsory, these payment terms are usually at the beginning of the invoice.

Format #2

The other format is more lengthy by comparison.

These terms and conditions basically list down the essential parts of a contract and look something like this:

Such invoices are usually created when requesting advance payment, so as to remind the client what work conditions and payment terms have been set in place before they undertake the project.

See also

How to write a perfect invoice and have all your accounting docs in order

Why do we need payment terms and conditions?

Aside from helping out the accounts department, adding payment terms to your invoice has multiple benefits. Some of them being:

1. They help align expectations

When you write payment terms, you can reinforce the expectations that were already stated in the contract or were based upon a verbal agreement.

Having these expectations written on paper (or digital record) serves as a reminder for both parties and helps deliver payment, fees, and late charges, all within the requested timeline.

2. They accelerate steady cash flow

Writing down payment terms helps clients process payments faster, which in turn, results in better cash flow for the billing party.

Once the cash starts rolling in, they know which resources to allocate the money toward.

3. They protect you from losses

Suppose you’re a new business owner who’s opened a bakery.

You’ve got everything set in place and ready to roll, but you’re relying on a payment from a client to buy a few pieces of equipment.

If that payment doesn’t arrive in time, you’d be looking at huge losses, such as money spent on rent and missing out on client orders.

So, to protect yourself from a hypothetical scenario like that becoming reality, it’s best to write out payment terms on the invoice, so that even if you’re paid late, you’re reimbursed in late fees.

4. They address repercussions

Payment terms also tell your clients exactly what repercussions are in place if they fail to pay on time.

For example, you might charge them interest or a late fee. Or if they put in a cancellation request, you can request a kill fee.

Or, if clients don’t end up paying or if they cause consequential damage, you could be justified in taking them to court and have them pay attorney’s fees (it goes without saying, the repercussions need to be agreed upon in the contract or need to be in place with all applicable law).

Why invoice terms matter for small businesses and freelancers

Having clear invoice terms and conditions help small businesses and freelancers get paid on time, avoid disputes, and help keep professional relationships with clients.

As a small business or freelancer, it’s always a good idea to have expectations around payment timelines, fees, and responsibilities set upfront. This way, you’ll have less confusion, you’re income will have more protection, and you’ll establish credibility. This is especially important if you don’t have a large legal or accounting team to use as a resource.

Create profesional invoices fast with PandaDoc

What terms and conditions should be on an invoice?

Alright, this is where we start getting into the details of what invoice terms and conditions actually look like. Remember, these are meant to set expectations around payment and help prevent any misunderstandings in the future.

You can think of them as the fine print that will answer questions before the client even has to ask.

Let’s start with the bare minimim of what your invoice terms and conditions should cover:

Payment due date

This is one of the first things that a client will need to know: when exactly payment is expected. This could be “Net 30,” “Due upon receipt,” or some other specified calendar date.

Remember, the clearer you are in your terms, the easier it will be for your clients to follow through. Plus, you’ll have an easier time following up, if needed.

Accepted payment methods

Clearly list out how your clients can pay you. This could be a bank transfer, credit card, check, online payment platforms, etc. This will get rid of friction and speed up the payment process.

Late payment fees or early payment discounts

Clearly state whether you charge interest or late fees on overdo invoices. Some poeple also include incentives to pay early, like a small discount. Either way, you should set these expectations from the beginning so you can avoid any awkwardness (or disputes) later.

Description of goods or services

Make sure your invoice clearly describes what the client is actually paying for. Even if it’s short, this description can prevent disputes later on. Plus, it will make sure the invoice aligns with your original agreement.

Additional policies or references

If you have any other policies regarding refunds, cancellations, or dispute resolution, include those as well. Or, you can reference a broader contract or terms document. This might be especially relevant for ongoing or higher-value work.

Important payment terms you need to know

Let’s be real: the corporate world is a world full of jargon.

Also real: to maintain professionalism, you need to know, or at least be familiar with, this jargon with respect to you getting paid.

So, let’s put our best professional foot forward and take a crash course on the popular payment terms and jargon you need to know about.

- Net-X Days: Net-X refers to X number of days you’re expecting payment. For example, if you write Net-0, you’re expecting prompt payment. Similarly, if you write Net-30, you’re expecting payment within 30 days.

- MFI: MFI stands for “month following invoice.” For example, if you write 15 MFI, it means you want payment on the 15th of the next month after you issue the invoice.

- PIA: PIA is short for “payment in advance.” What it basically means is that you’re expecting upfront payment before you begin working on the project. If you write 50% PIA, it means you want a 50% upfront payment. Similarly, 100% PIA refers to 100% advance payment.

- CIA: CIA, also known as cash in advance, means you want your clients to pay in cash in advance. The advanced payment would ideally be of an X% (e.g., 30% CIA, 50% CIA, 70% CIA, etc.).

- Upfront: Upfront means you want the payment before you begin working on a task for the client. Upfront payments are usually treated as a deposit, so there’s less of a worry of non-payment later on.

- COD: Short for “cash on delivery,” COD means you want payment in as soon as the product/service is delivered by you. Because clients may choose not to pay in the moment, many companies prefer not to opt for the COD method.

- EOM: EOM means “end of month.” If an invoice says “payment at EOM,” it means they’re expecting payment by the end of that month.

- Upon Receipt: Upon receipt means immediate payment. So, as soon as you get the invoice, you process the payment (i.e., within the timeframe of a day).

- Cash Account (no credit): What this means is you expect a cash payment, and you’re not willing to offer any credit to your clients.

- Cash Account (letter of credit): This is the opposite of “cash account (no credit)” because here, you are expecting cash payment, but you will also accept a letter of credit from a reputable bank.

- CWO: CWO, short for “cash with order,” means that you expect payment of all the products/services as soon as the order has been placed.

- CND: The full form of CND is “cash before delivery.” What it means is that you’re expecting some down payment in order to begin working on the project that’s been assigned to you.

- CBS: CBS, abbreviated for “cash before shipment,” means you want a deposit before you ship the product to safeguard yourself against non-payment.

- Accounts Receivable: Accounts receivable refers to the balance total you’re owed by a client. For example, if New Client A owes you $500, then your accounts receivable for that client would be $500.

- N/N Net-X Days: The “N” and “X” stand for numbers, and N/N Net-X days refer to payment deadlines and discounts. For example, if it would say 2/5 Net-20 days, it means you’re expecting payment within 20 days, but if the client processes payment within 5 days, you’ll give them a 2% discount on the entire invoice amount.

- Waiver: Waiver refers to waiving an amount or a claim. For example, if you give a waiver on the security deposit, it means you’re not expecting a security deposit before working on a project.

- Others: There are other important terms that are not-so-commonly used in invoices, but are still important to know about, such as RD (rollover deposit), contra, early payment, purchase order, etc.

Invoice payment terms and examples

Now that we’ve covered the basics of invoice terms and conditions, let’s get to the important topic — examples (aka, the entire reason why you started reading this article).

While you can change your payment terms depending upon the project you undertake, the contract you have in place, and on a case-by-case basis, here are a few examples you can refer to.

Payment timing

These are terms that define when payment is due. They also help avoid confusion around the deadlines, which is essential for avoiding late payments.

Net payment terms

- Definition: This specifies a set number of days after invoice issuance that the payment needs to be received.

- Why it matters: It standardizes expectations and lets both sides plan ahead.

-

Sample clauses:

- “According to our [insert name] agreement, payment follows a Net-7 days cycle.”

- “Please send payment within 30 days of the invoice date (Net 30).”

End of month (EOM)

- Definition: Payment has to be made by the end of the month in which the invoice is issued.

- Why it matters: It aligns billing with monthly accounting and reporting cycles.

-

Sample clause:

- “Request payment by EOM.”

Upon receipt

- Definition: Payment is due as soon as the client receives the invoice.

- Why it matters: This leads to faster payments for one-off jobs or smaller invoices.

-

Sample clause:

- “Payment is to be made upon receipt.”

Upfront and staged payments

These are terms about how and when partial payments are made before or during a project. This is important when it comes to managing risk and covering costs for the project.

Upfront deposit

- Definition: A percentage of the total amount is due before work begins.

- Why it matters: This helps cover initial costs and makes sure your client is committed to the agreement.

-

Sample clauses:

- “A 50% upfront payment is required to begin working on the [insert name] project.”

- “To begin working on the order, we’ll need a 15% PIA (payment in advance).”

Milestone billing

- Definition: Payments are tied to project phases or deliverables instead of paying the full amount up front.

- Why it matters: This is helpful for longer or multi-stage jobs because it keeps cash flowing as work progresses.

-

Sample clause:

- “Payments will be invoiced upon completion of the following milestones: [list phases].”

Penalties and incentives

These are terms that explain what would happen if payments are late, or if you make an early payment. Both of these can motivate a timely payment.

Late fees

- Definition: A charge will be applied if the invoice isn’t paid by the agreed due date.

- Why it matters: This prevents late payments and compensates for necessary follow-ups.

-

Sample clause:

- “If unpaid by Net-30, a late fee of 20% on the invoice amount will be applicable (days will be counted based on the invoice date).”

Early payment discounts

- Definition: This would reduce the amount owed if the client pays before the due date.

- Why it matters: This term encourages faster payment; plus, the client is happy to recieve a discount.

-

Sample clause:

- “A 2% discount applies if payment is received within 10 days of the invoice date.”

Order and delivery conditions

These terms help protect your business during fulfillment because they outline payment expectations to requirements for delivery or client authorization.

Client approval before delivery

- Definition: This term requires client sign-off or form completion before shipment or delivery.

- Why it matters: It helps confirm authorization and reduces disputes over deliveries.

-

Sample clause:

- “[Insert client name]’s signature on the declaration form is required to ship the product [insert reference number].”

Cash on delivery (COD)

- Definition: Payment needs to be collected at the time the product is delivered.

- Why it matters: The payment risk is attached to the moment of delivery.

-

Sample clause:

- “This is a COD order. Payment may be given to the delivery person.”

Cancellation, no-show, and other policies

There are general terms and conditions that can appear alonside payment terms that address what happens when a job or project doesn’t go as planned.

Cancellation or kill fees

- Definition: A fee is charged if a client cancels after work is scheduled or started.

- Why it matters: You get compensated for lost time and resources.

-

Sample clause:

- “A kill fee of [insert amount] is required for the cancellation of order request [insert reference number].”

No-show or late cancellation terms

- Definition: Details any charges that occur if a client misses an appointment without appropriate notice.

- Why it matters: You can better protect your schedule and get compensation for unsold time slots.

-

Sample clause:

- “A no-show fee of [insert amount] applies if the client fails to appear for the scheduled appointment without at least [insert time period] notice.”

You can use combinations and variations of these payment terms in whichever way best suits your business needs.

Also, in cases where you’re requesting advance payment and want to add multiple terms and conditions to backstop project expectations, you can write payment terms below the itemized list.

These terms and conditions can include details about the warranty, insurance, payment structure, liability, force majeure, working additions, payment for additional work, time tables for the work to be completed, and other such details.

Alternatively, you can also use PandaDoc’s template library to refer to a few more examples on how to write payment terms and conditions.

See also

16 best invoicing software options to facilitate your payment process

Freelance invoice terms

Because freelancers typically work with different clients, project scopes, and timelines, clear invoice terms are a necessity. You want to get paid on time and avoid misunderstandings.

Here are some common freelance terms to include:

Upfront deposits

It’s common to request partial payment before starting work to reduce risk. You might include a clause like “A 50% deposit is required before work begins.”

Net payment terms

Net 7, Net 14, or Net 30 are common terms for projects, which could appear something like: “Payment is due within 14 days of the invoice date (Net 14).”

Milestone billing

Longer projects might require payments to be tied to deliverables. In this case, you could include a clause like, “Payment will be invoiced upon completion of agreed project milestones.”

Late payment fees

Late fees will encourage timely payment, so include a clause like, “A late fee may apply to overdue invoices.”

Cancellation or kill fees

Kill fees can help freelancers if a project is canceled after already starting the work. It covers time already spent. A sample clause would be: “If the project is canceled after work has started, a kill fee will apply.”

Small business invoice terms

Small businesses also benefit from clear, consistent invoice terms so that they are easy for customers to understand. As always, use simple language and standard payment schedules to avoid confusion and speed up payments.

Here are some common invoice terms to include if you’re a small business:

Standard payment schedules

Net 15 or Net 30 terms are widely used and easy to manage, which could look like, “Payment is due within 30 days of the invoice date (Net 30).”

Accepted payment methods

Make it easier for your customers to pay with a clause like, “Accepted payment methods include credit card, bank transfer, or check.”

Refund or return policies

If you offer refunds or returns, state conditions like, “Refund requests must be submitted within 14 days of purchase.”

Late payment policies

Have a simple late fee policy to encourage your customers to make payments on time. Include a clause like, “Late payments may be subject to a fee.”

Delivery or fulfillment terms

If you’re a product-based small business, you might require payment before delivery. In that case, you can include a clause like, “Orders will be shipped once payment has been received.”

How to write invoice terms and conditions step by step

Don’t be intimidated to start writing your invoice terms and conditions. Here’s a simple breakdown or how to do it, step by step:

1. Start with a baseline contract

It’s a good idea to use the contract you already have with your client that outlines payment structures and responsibilities as a baseline. It will help you write your invoice terms so that you and the other party will be aligned on what you’ve already agreed upon, and what you’re billing for.

2. Define payment timing in plain language

You need to decide when exactly you expect to be paid, and make sure it’s written clearly. Avoid awkward legal phrasing and sticke to everyday terms. For example, “Payment is due within 30 days of invoice dates.” This simplicity will reduce possible confusion.

3. List acceptable payment methods

List all the ways you will accept money, whether that’s a bank transfer, credit card, check, etc. This will help the client understand their options from the get-go.

4. Add incentives or penalties

Decide whether you want to reward early payments or penalize late ones. This could look like offering a 2% discount if it’s paid within 10 days, or perhaps adding 1.5% interest per month that the payment is overdue. This will set expectations upfront.

5. Include any necessary delivery or scope notes

If your invoice includes physical goods or services that come in phases, you can tie the payment terms to those types of milestones. For example, you could say “Final payment is due upon delivery of all items listed.” This will connect the invoice to the actual performance of the task/service.

6. Be clear and concise

Don’t be tempted to over-explain. Make sure your terms are written clearly, and avoid using any jargon. Assume the client reading this doesn’t have an accounting degree.

7. Review and reuse

Once you come up with solid terms that work for you and your business, save them in your invoice template library so you don’t have to start from scratch every time you get a new client.

Best practices to consider

1. Create a contract to accompany invoices

Here’s the thing: invoices by themselves are not legally binding.

But, if you accompany them with a contract, then yes, they can be binding.

So, to ensure that your invoices are paid on time, and that expectations and responsibilities are in alignment with both parties, it’s best to create a contract with an invoice.

You can include details like payment timelines, due dates, warranties, legal remedies, work conditions, project scope, responsibilities of both parties, and other such details.

In sum: sending contracts is the first step to getting paid.

You can refer to a few contract templates by PandaDoc to get a better understanding of how you should construct yours.

2. Send invoices in a timely fashion

If you’re expecting clients to pay your invoices on time, it’s always best to extend the same courtesy and send those invoices on time.

Most businesses create invoices at the end of the month or once they finish certain project milestones, but you can discuss which timelines work best for your clients and send invoices accordingly.

3. Use simple-to-follow language

There’s a slight difference (see if you can spot it) between “I ate, uncle John” and “I ate uncle John.”

But this difference means two widely different things (and may impact future family gatherings).

Instead of using words or sentence structure that might complicate things for you, it’s best to use a simple and straightforward language so your client knows exactly what you mean.

4. Don’t miss out on important details

Before you send your client an invoice, make sure it doesn’t miss any important details.

For example, the invoice date, billing address, total amount, itemized list, project names, quantities, etc., so that there are no delays and back-and-forth, and you can get paid on time.

One way to ensure that you never miss out on any details is to keep ready-made templates and content libraries handy, which you can use at a moment’s notice.

To quickly create templates and content libraries, you can refer to our reserve by going to Resources > Templates > Invoices, or you can create them from scratch with the PandaDoc editor.

How can PandaDoc help?

Creating invoices and populating them with payment terms serve one particular purpose — to get paid on time.

However, you may not have the time to create the formal invoices you need.

This is a common phenomenon with many small businesses and freelancers who don’t have a separate accounts department handling invoices for them.

However, what if we told you that you could spend less time creating invoices, see better productivity rates, use ready-made templates, and track invoices to see insights?

You’re in luck, because PandaDoc lets you do just that — you can decrease time spent creating invoices, improve close rates, increase productivity, use a library of templates, and track invoices.

To learn more about what PandaDoc has to offer, try PandaDoc or arrange a free call with our representatives — they’ll happily guide you through what PandaDoc can do for you and your business!

Disclaimer

PandaDoc is not a law firm, or a substitute for an attorney or law firm. This page is not intended to and does not provide legal advice. Should you have legal questions on the validity of e-signatures or digital signatures and the enforceability thereof, please consult with an attorney or law firm. Use of PandaDocs services are governed by our Terms of Use and Privacy Policy.