Nebraska Apartment Lease Agreement

You can download our legally binding Nebraska Apartment Lease Agreement template to adhere to state laws.

Finish your demo booking

Looks like you haven't picked a time for your personalized demo. Pick a time now.

Select date and time

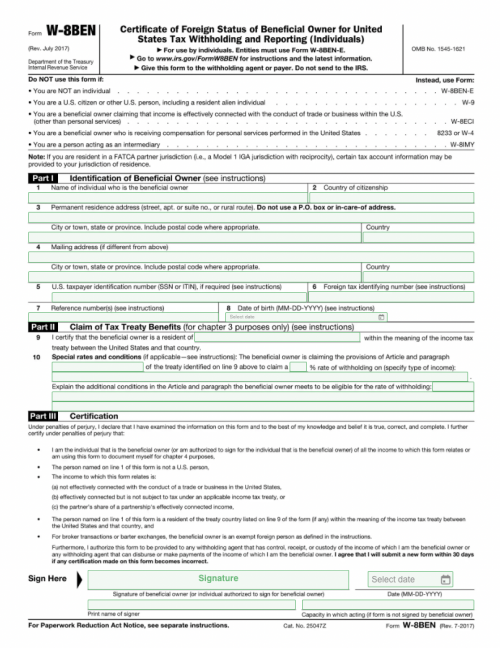

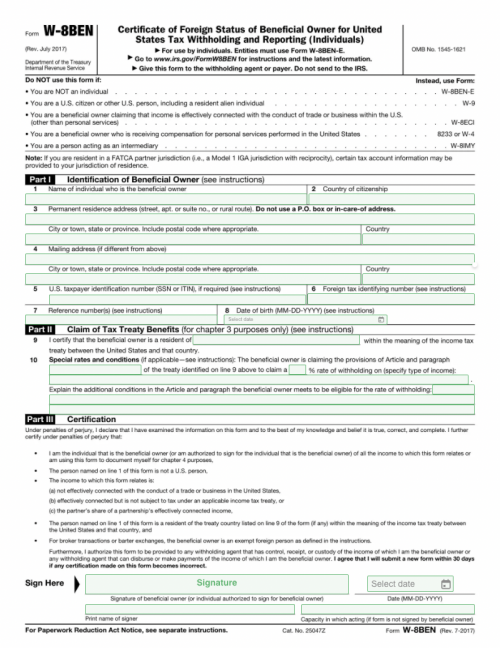

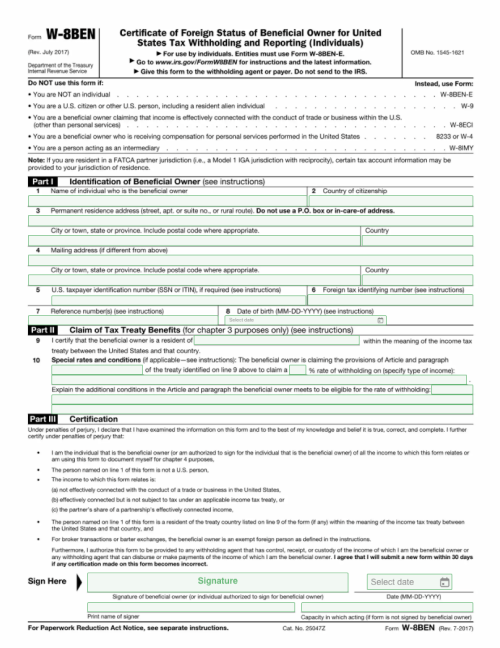

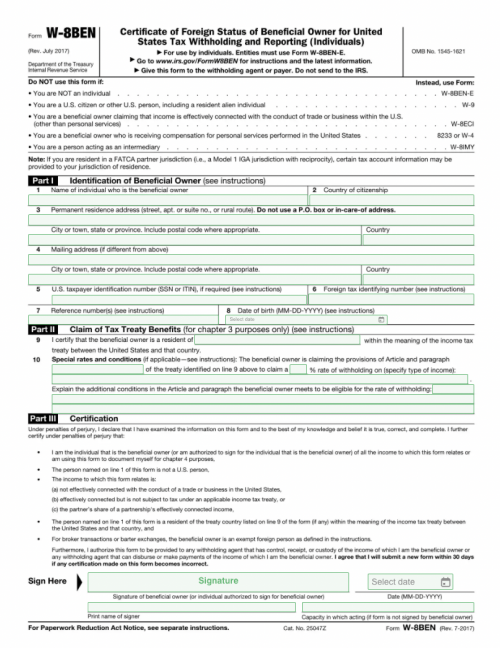

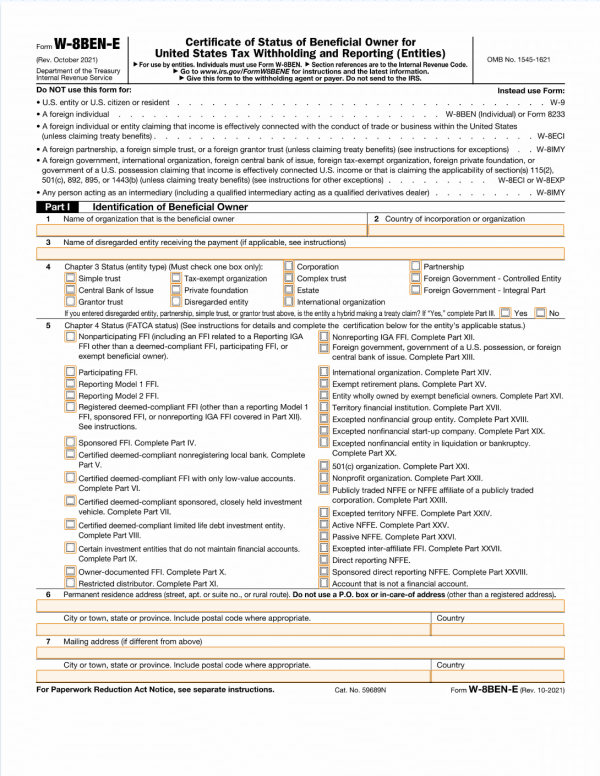

The W8-BEN Form is a form required by the IRS, similar to the W9 form that employees and subcontractors in the United States must submit to employers

Get your W-8BEN forms’ versions from 2017 to 2023

The IRS requires that taxes be paid on income paid to entities outside of the United States.

Typically, this rate is 30%, but it can differ from one foreign country to the next. The W8-BEN must be filled out by a non-US entity receiving compensation from a US entity.

It ensures that the individual or company issuing payment knows to withhold taxes from payment, and to subsequently pay those taxes to the IRS.

If you’re a company or individual paying non-US entities, you will be held liable by the IRS for the taxes that should be withheld from payments you send them, which makes it important to have a W8-BEN on file for these entities.

The W8-BEN is a single page form with three sections:

Like the W9, the W8-BEN is not submitted to the IRS. Instead, it’s submitted to the US entity issuing payment, and they keep it in their records.

If you’re a company outside the United States and receiving payments from US entities, you’ll use the W8-BEN-E version of this form instead of the standard version.

Nebraska Apartment Lease Agreement

You can download our legally binding Nebraska Apartment Lease Agreement template to adhere to state laws.

Group Contract Template

A group agreement is a clear set of guidelines on how your group will handle discussions, meetings, and sensitive information raised in the group setting.

Inbound Services Agreement Template

This document authorizes two or more corporations to work together through the licensing of intellectual property. Check out PandaDoc’s Inbound Services Agreement Template below to make your own license consensus.