Internship Contract Template

The agreement developed based on this PandaDoc Internship Contract Template comes to be a lawfully binding consensus when electronically signed by all the parties.

Finish your demo booking

Looks like you haven't picked a time for your personalized demo. Pick a time now.

Select date and time

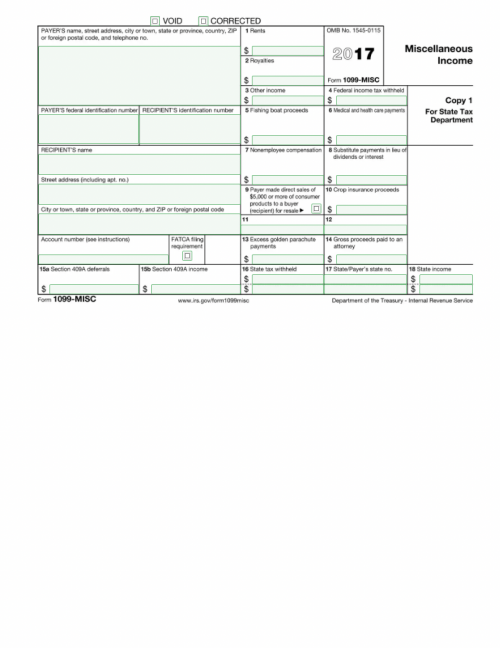

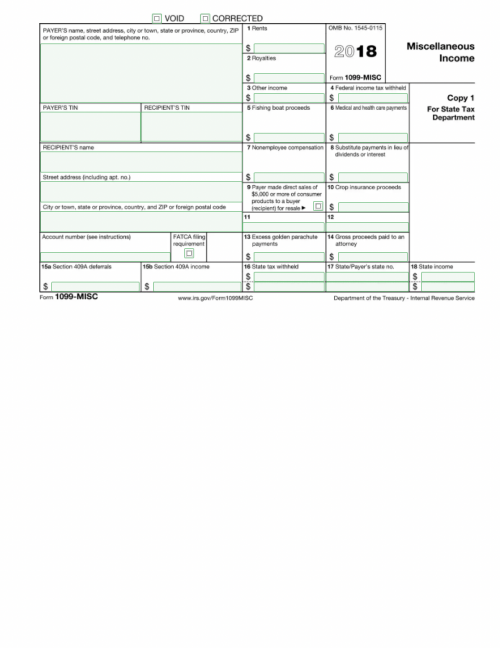

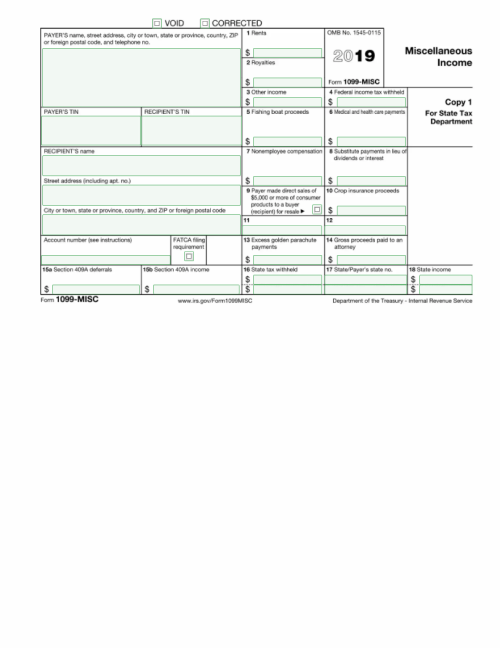

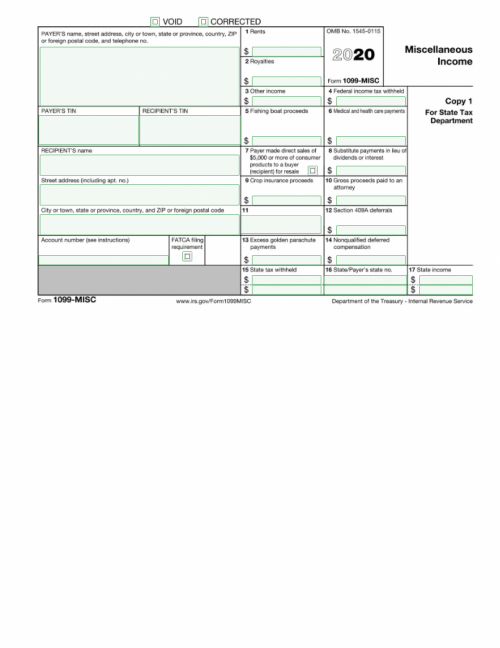

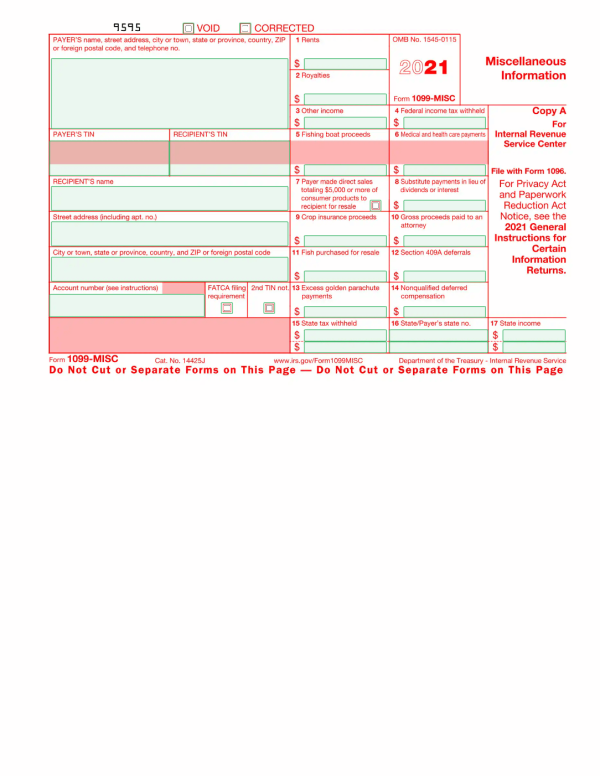

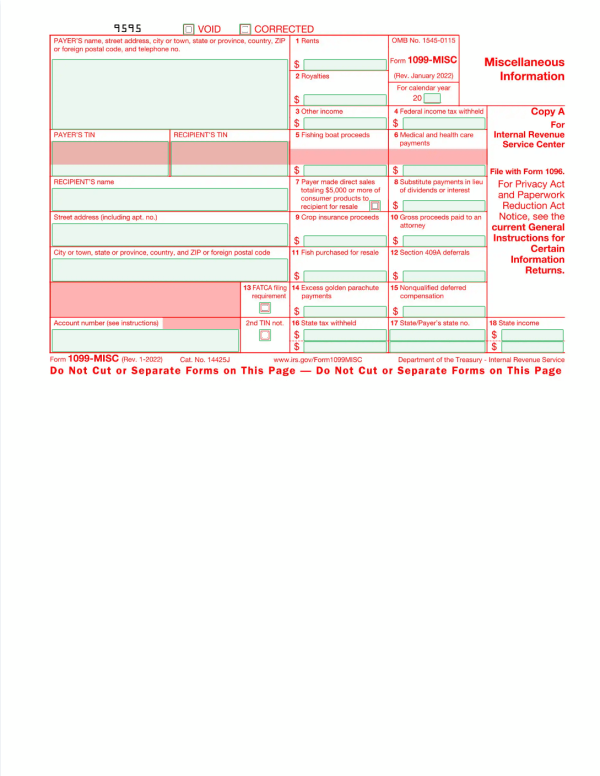

The 1099-MISC Form is an IRS tax form used to report payments made from a company to contractors or consultants.

Get your 1099-MISC forms’ versions from 2017 to 2023

The 1099-MISC is an 8 page document, but there’s only one form that needs be filled out (the document includes several copies of the same form, which are filed in the Payer’s records, sent to the Payee, and submitted to both the IRS and your state’s tax department.

When completing the form, you’ll need to identify yourself (the Payer), the consultant or contractor you’ve paid (the Recipient), and the details of amounts you’ve paid over the past year.

As the Payer, you’ll need to file the 1099-MISC form with the IRS and your state’s tax office by the deadline, which varies depending on the year and filing method chosen.

You’ll also send the “Payer” section of the form to the listed “Recipient” so that they may complete their annual tax return.

Many 1099-MISC Forms found online use the IRS’ informational copy, with the second page printed in red. Do not use this copy for your filings or you’ll be subjected to penalties by the IRS.

You’ll need to complete and file a 1099-MISC if:

Internship Contract Template

The agreement developed based on this PandaDoc Internship Contract Template comes to be a lawfully binding consensus when electronically signed by all the parties.

Startup Pitch Deck

Present your startup business and attract investments using this free startup pitch deck template.

Website Development Quote Template

Do you need a document that can contemplate the prerequisites in terms of functionality that is required for your website? Use this Website Development Quote Template.

Robotic Process Automation (RPA) Proposal

Elevate your IT service sales with our Robotic Process Automation (RPA) proposal template.